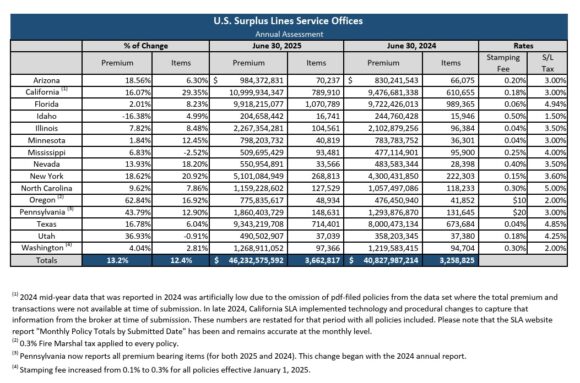

Surplus lines sector continues to grow with mid-year premium reaching $46.2 billion from the 3.7 million items filed so far in 2025, according to data from U.S. surplus lines service and stamping offices in 15 states.

These figures represent a 13.2% increase in premium and a 12.4% rise in items compared to the same period in 2024, the 2025 Midyear Report revealed. For the same six month period in 2024, the report showed premium at $40.8 billion from 3.3 million items filed. In total, 2024’s results of $81.6 billion in premium represented growth of 12.1% as reported.

The 2025 midyear report organizes the stamping office data by line of business, broken down by both premium and items filed.

Commercial liability and commercial property coverage continue to dominate market share trends in the E&S market, accounting for $16.9 billion in premium and 36.6% of total share for liability – non-professional, and $15.7 billion and 34.0% of total share for property at midyear 2025.

Auto liability and residential, homeowners and other personal property continue to grow faster than other lines in the surplus lines segment but still comprise a relatively small proportion of the overall surplus lines segment among the stamping office states (3.6% and 5.3%, respectively).

The report presents comparative analysis of the 2025 and 2024 surplus lines market, highlighting nine key lines of business: auto liability, auto physical damage, disability/A&H, inland marine, liability (non-professional), multiperil, professional liability, property, and residential/homeowners/other personal property.

In collaboration with stamping offices in 15 states (Arizona, California, Florida, Idaho, Illinois, Minnesota, Mississippi, Nevada, New York, North Carolina, Texas, Oregon, Utah, Pennsylvania, and Washington), the report maps each state’s coverage codes into surplus lines premium and transaction data for these nine lines of business.

The growth of these lines underscores the essential role of the surplus lines industry as a solution where the standard market’s appetite evolves.

In Arizona, disability/A&H and auto physical damage grew significantly, said Edward Dresselhuys, executive director of the Surplus Line Association of Arizona. “Disability/A&H, up 68.7%, and auto physical damage, up 57.0%, grew substantially but still constitute relatively small pieces of the Arizona surplus lines market,” he said. “Our largest lines, general liability and property, grew modestly but professional liability was up 36.6% which significantly drove growth.”

Idaho was the only state that saw a decrease in premium through mid-year 2025, largely driven by drops in liability and commercial property lines. Carrie Negrette, Executive Director of the Surplus Line Association of Idaho said that while Idaho is down 16% through mid-year 2025, putting that into context of recent growth, Idaho premium volume is still up 82% since mid-year 2022.

Tim Turner, CEO of Ryan Specialty and chairman of RT Specialty, told Insurance Journal that the midyear report is consistent with growth seen in RT’s business. Turner said that RT is continuing to see double digit increases in premium and anticipates the organization will write in excess of $30 billion in premium in 2025. RT continue to see 20%-plus growth annually, due to niche business “firming” in some lines of insurance, Turner said. “One area that hits home for most of us would be social and human services, which encompasses everything from hospitals to nursing homes to assisted living to allied health facilities,” he said. “That segment of business is just getting harder by the day.”

The 15 state surplus lines stamping and service offices are non-governmental entities that help facilitate compliance with surplus lines insurance regulations and tax filings as well as additional services for their respective memberships.

Topics

Trends

Excess Surplus

Pricing Trends

Interested in Excess Surplus?

Get automatic alerts for this topic.